How to Dispute a Collections Notice: A Complete Guide

If you get a collection notice you don't believe is valid, you need to know the smartest way to respond.

Last updated Aug 24, 2023

All About Cookies is an independent, advertising-supported website. Some of the offers that appear on this site are from third-party advertisers from which All About Cookies receives compensation. This compensation may impact how and where products appear on this site (including, for example, the order in which they appear).

All About Cookies does not include all financial or credit offers that might be available to consumers nor do we include all companies or all available products. Information is accurate as of the publishing date and has not been provided or endorsed by the advertiser.

The All About Cookies editorial team strives to provide accurate, in-depth information and reviews to help you, our reader, make online privacy decisions with confidence. Here's what you can expect from us:

If you don’t pay a debt, the creditor can try to collect from you or it could sell your debt to a debt collection agency.

When creditors or third-party debt collectors want to try to obtain money from you to satisfy a debt, they typically are required to send you a collection notice. Unfortunately, there are times you may receive this type of notification for a debt you don't believe you owe. If that happens, you need to know how to dispute collections so your credit isn't damaged and you don't face legal repercussions, such as a potential lawsuit.

Whether you're disputing collections because your identity was stolen or because you believe creditors made a mistake and are trying to collect money you don't owe, this guide can help you to understand the process so you can protect your rights and avoid serious harm to your financial future.

Having accounts in collections could damage your credit score, and creditors can take steps such as suing you in order to collect against you — if you legitimately owe money. This is why it's so crucial to respond aggressively and quickly if you receive a collection notice you believe is invalid.

It can be complicated to figure out how to dispute collections, but these are the key steps you'll typically need to take.

Under the Fair Debt Collection Practices Act, debt collectors must provide written notice about your debt within five days of contacting you. This notice must include:

It is important to pay attention to the details the collector provides and to respond very quickly to the collection notice if you hope to dispute it. This is especially essential if someone has used your personal identifying information to improperly take out loans or other credit in your name, and now you're facing collections for a debt you don't owe.

Once you receive the collection notice, you can review your own records of what you borrowed and what payments you made and compare them with what the collectors say you owe. Doing this will enable you to be armed with the details necessary to determine whether the debt is valid and to dispute the collection if it isn't.

It's helpful to have all information from the collector in writing so you can keep detailed records of when you were notified about what you owed and when you responded.

After you receive a collection notice, the next step is to respond to it.

According to the FDCPA, consumers have the right to dispute the debt by notifying the collector within 30 days.

After receiving a debt dispute letter from a borrower, the collector typically must cease collection of any disputed portion of the debt until obtaining and providing verification of the debt. This verification could include any or all of the following information:

Creditors only must provide this proof if you ask for it, which is why writing a debt dispute letter and sending it within 30 days is so critical.

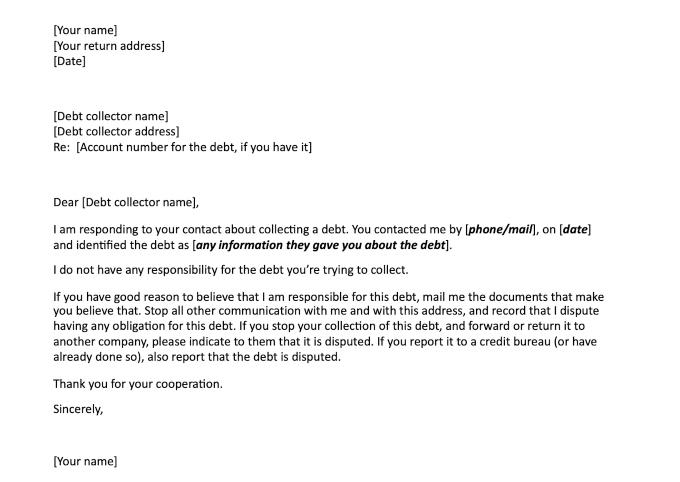

The good news is that you can find sample debt dispute letters online from many sources. For example, here is a sample debt dispute letter from the Texas State Law Library. The below sample dispute letter is also another option from the Consumer Financial Protection Bureau. You can copy this letter and fill in the specific details.

The CFPB also has many additional sample letters, including correspondence appropriate for the following circumstances:

You should always dispute a debt in writing and keep records of the information. Be sure to date your dispute letter to prove you sent it in time. And also consider sending it certified mail with a return receipt requested so you have proof the letter was received by the collector.

Debt collectors cannot report disputed debt to credit reporting agencies, so you can protect your credit history by acting quickly if the debt is not valid.

There is no specific time period during which collectors must respond when you dispute a collection notice, though the collector typically must discontinue certain collection activities until it provides the required proof in response to your letter.

If the collector does respond, you can use the information it provides to determine whether the debt is yours to pay. If your identity was stolen, you can move forward with filing a police report and providing the collector with proof of the identity theft. If the debt collection is legitimate, you will need to decide on your best course of action.

If the debt collector provides proof that you owe the debt, you will have to decide on your next steps. You should:

Make sure the debt is still collectible

There is a statute of limitations on collecting debt. Once the time limit has passed, any collection activities are time-barred and collectors can't proceed with legal action against you to try to recover the money you owe. The specific length of time the statute of limitations runs can vary. However, if you make a payment, the clock can reset. As a result, you'll want to avoid paying any money to collectors without confirming the debt is still collectible.

Reach out to your creditors

If you legitimately owe a debt and the statute of limitation hasn't run out, you'll want to resolve the issue. If you hope to make payments to deal with the debt and avoid potential legal action against you, it's a good idea to contact your creditors to explore your options. Collectors are often willing to accept a lump-sum payment to settle your debt, especially if the collectors bought the debt from the original creditors for pennies on the dollar. Creditors or collectors may also be willing to negotiate a payment plan to try to recover some of the money owed.

Consider getting help

Credit counseling services or bankruptcy attorneys may provide you with assistance negotiating with creditors or exploring your options if you have debts you cannot pay.

Remember, there are limits to what creditors can do. In most cases, they cannot take your home or seize federal benefits, and some states prohibit the garnishment of your wages for any debts other than back taxes, defaulted student loans, or unpaid child support. So be sure you know your rights before you decide whether to begin making payments or how much to pay.

You have the right to request that the debt collection agency not contact you.

Collection agencies can still proceed with certain collections activities, including filing a lawsuit, if you legitimately owe a debt and the collections activities are not time-barred. Although you may be tempted to just ask them to discontinue communications, this typically will not solve the underlying issue if you legitimately owe money.

Understand your rights

Even if you do legitimately owe money, though, it is important to understand your rights as well as the limitations imposed on collectors under the FDCPA. For example, collectors cannot falsely threaten to pursue legal action or harass you, they cannot call you too early in the morning, and, as mentioned above, they cannot continue to call you if you request they stop.

Keep records

Not only should you know your rights under the FDCPA, but you should also be sure to keep records of any dealings with collectors so if they violate an agreement or break the law, you will have proof of it. If they don't follow the rules, you could report bad practices to the CFPB and/or your state attorney general, and you may wish to speak with an attorney for legal advice about your rights.

Review credit reports regularly

You should also keep tabs on your credit reports to find out if collectors are reporting any negative information or if there are any other credit report errors. If incorrect information shows up on your credit report, you can dispute it with the three major credit reporting agencies: TransUnion, Equifax, and Experian. Under the Fair Credit Reporting Act, the credit bureaus are required to correct or delete inaccurate information.

Collection accounts can be removed from a credit report if they're invalid by filing a dispute with the credit bureaus. Even if the debt was valid, you can still contact the collector and ask that they remove the information. Debt collectors or creditors do not have to remove accurate collections notices but may do so as a courtesy if the account has been paid in full. This is sometimes referred to as a goodwill deletion.

Collectors can pursue legal action against you to try to collect unpaid funds, and that can negatively affect your credit, so it is worth disputing a collection if you don’t owe the money. Disputing accurate collection accounts isn’t worth the effort because an investigation will likely reveal their validity and collectors will be allowed to proceed with collection efforts.

If you get a collection notice, you can request the collector verify the debt, or you can contact the collector to work out a payment agreement. Collectors must verify disputed debts and cannot continue collection activities without providing the requested verification. If you do owe the debt, working out a payment plan could be the best course of action to limit damage to your credit score.

Getting a collections notice can be frightening, but you have options. You should make sure the debt is valid and take action to dispute it within 30 days if you don’t believe you owe the money. You should also make sure you know your rights under the FDCPA so you can take appropriate actions if collectors violate your rights.